CCTV News:Buying a house requires a loan, and everyone has become accustomed to it; Now the cemetery can also get a loan. A few days ago, a cemetery in Kunming launched a "cemetery mortgage loan" with a maximum loan of 200,000 yuan and a term of 10 years.

According to the staff, this is a pure credit loan and no mortgage is needed. Male age+loan period is not more than 75 years old, and female age is not more than 65 years old. The down payment is 20%, and the loan interest rate is 9%. If there is a guarantor, you can also achieve a down payment of 0. If it is handled, it can be completed within one week at the earliest.

However, once this "cemetery loan" was launched, it caused an uproar. Finally, the bank announced that it would cancel the credit project and ended in a hurry.

Qiqi’s loan can be more than this one. Not long ago, the advertisement of "bride price loan" launched by Jiangxi Jiujiang Bank rushed to the hot search, and the related recommendation language made people stunned: "Don’t worry about the bride price, lend a stable happiness." The poster shows that the "bride price loan" can be loaned up to 300,000 yuan, up to one year, and the annual interest rate is as low as 4.9%, which is used for wedding travel, car purchase, jewelry purchase and so on.

After the "bride price loan" rushed to the hot search and triggered a hot discussion on the Internet, the supervision intervened in the investigation. At present, the bank issued an apology statement, saying that the person directly responsible had been suspended.

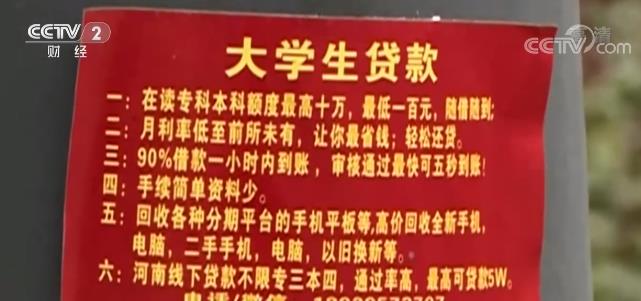

In addition to cemetery loans and bride price loans, there are down payment loans for buying a house, second child loans for giving birth to a baby, rent loans for renting a house, home improvement loans for decoration, beauty loans for medical beauty, travel loans for going out, and all kinds of wonderful loans give people the illusion that there are loans wherever there is demand.

In addition to loans for specific projects, there are also loans for different groups of people. For example, tailor-made gardener loans for teachers, reporter loans for journalists, angel loans for medical staff, chef loans for chefs and so on. As long as you have a demand, you can definitely find a loan tailored for you.

Instead of welcoming the expected enthusiasm, these fancy loans full of gimmicks attracted criticism from ordinary people.

Consumers don’t pay the bill, why do banks have so many wonderful loans? The reason is that in the past two years, with the suspension of offline cross-regional operations of small and medium-sized banks, the restriction of online cross-regional lending, and the sinking of consumer loans, the performance pressure has become increasingly heavy. Under the pressure of business, in 2021, products such as "bride price loan" and "cemetery loan" which are known to be controversial began to take off.

Yue Yunsheng, Secretary General of Rules and Regulations Committee of Beijing Lawyers Association:The starting point of a bank must be to increase its income, and what products the bank designs. I think this is understandable. The key is that the premise is to comply with the laws and regulations, and the key is to conform to public order and good customs. You can’t design some products that will corrupt the social atmosphere.

The data shows that these wonderful loans are indeed slightly higher than the annual interest rates of other consumer loans. For example, "bride price loan" can buy a car, and its loan interest rate is 4.9% per year, while the average annual interest rate of consumer loans for automobiles may be only about 3%.

In addition to making money, banks’ competition for consumer application scenarios is also the reason for the endless stream of exotic loans.

Experts said that some loan scenarios in personal consumption have been occupied, such as mortgage and car loan. Therefore, banks have to find consumer application scenarios and make loans bigger, so various names have come out.

It is undeniable that with the intensification of competition in the financial market, the pressure on some financial institutions, especially small and medium-sized banks, has increased sharply in recent years. While competing for market segments, there are also some small and medium-sized banks that choose to go sideways and play special gimmicks.

Yue Yunsheng, Secretary General of Rules and Regulations Committee of Beijing Lawyers Association:Now, some of them may be scratching their edge, that is, the so-called public order and good customs, which are relatively vague with legal boundaries and moral boundaries after all. At this time, in order to be unconventional or gain a certain competitive advantage, banks always have to innovate something. The so-called innovation, whether in terms of innovation or innovation in marketing methods, is aimed at serving the purpose of making profits.

Wonderful loan "loan" does not come to consumption upgrade

What kind of problems are reflected behind these wonderful loans? Is it really to promote consumption upgrading, as the bank said?

Ms. Li from Changsha, Hunan Province, had a rhinoplasty operation in a plastic surgery hospital two years ago. At that time, due to the shortage of funds, the beauty hospital recommended her a "phased" loan platform.

According to the information provided by Ms. Li, her loan has been repaid in 24 installments, and all of them have been repaid at present. However, recently, she found that one of the two credit cards in her name had a reduced loan amount, and the other was directly suspended. After the investigation, I found that I had a serious bad credit record.

It is clear that the arrears have been settled, but there is an overdue amount of 5652 yuan on the credit transaction details, which makes Ms. Li puzzled.

Nowadays, there are still many serious consequences caused by beauty loans. Because Wuhan Xiaowang was unable to repay the loan after cosmetic surgery, he was taken by the intermediary to sell eggs and pay back the money.

I went to three hospitals in a row, and after 17 days of egg-promoting injections, the egg retrieval still ended in failure. When Xiao Wang came home, he felt unwell and suddenly fell into a coma, almost losing his life.

Micro-loans like this are everywhere in today’s society. An ID card and a mobile phone number can enjoy the treatment of advanced consumption, which seems to be convenient for the public, but it is hidden.

Central Bank: Individual financial institutions launch "wonderful loans" to touch the social bottom line.

In response to these wonderful loans, the central bank also responded yesterday (1 ST). Individual banks challenged social pain points under the banner of so-called financial innovation, guided residents to over-debt, and touched the bottom line of social public order and good customs.

Zou Lan, director of the Financial Markets Department of the Central Bank, said that individual banks, under the banner of so-called financial innovation, challenged social pain points, guided residents to over-debt, touched the bottom line of social public order and good customs, and broke away from their duties of financial services to the real economy. In fact, the essence of this kind of loans is consumer loans, and individual banks promote customers by making gimmicks, which also reflects the lack of service capabilities of some small and medium-sized banks.

Director, Financial Market Department, People’s Bank of China Zou LAN:We should promptly correct practices that violate public order and good customs and run counter to the state’s major policies.